您的钱归谁?美国遗产税与继承税深度揭秘

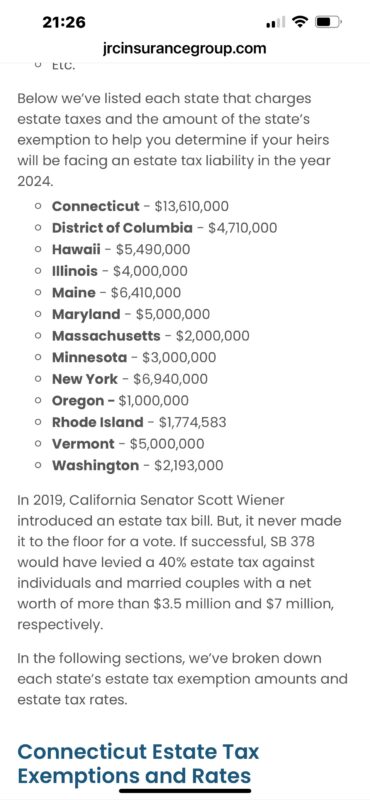

您的钱归谁?美国遗产税与继承税深度揭秘 随着财富传承成为越来越多家庭讨论的重点,了解不同州对遗产和继...

2024-04-20阅读(9884)赞 (24)

您的钱归谁?美国遗产税与继承税深度揭秘 随着财富传承成为越来越多家庭讨论的重点,了解不同州对遗产和继...

2024-04-20阅读(9884)赞 (24)

看中国 · 外国青年影像计划 中国那么大,一起看看吧 人们常...

2024-04-19阅读(8839)赞 (8)

4月已过半,之前连续的周末雨天不仅湿润了大地,也打破了不少小伙伴的出游计划。但好消息是,这个周末终于...

2024-04-19阅读(10405)赞 (40)

4月19日(周五),数十名谴责以色列在加沙的冲突中的行动者仍然在哥伦比亚大学的西草坪上搭起帐篷继续抗...

2024-04-19阅读(11609)赞 (12)

特斯拉因油门踏板可能在被踩下时卡滞而被命令召回近4000辆Cybertruck。监管机构表示,问题源...

2024-04-19阅读(9297)赞 (7)